Infibeam Avenues Ltd – Many of you have heard this script for the first time. 28th September 2018 was a black Friday for the shareowners of Infibeam Avenues Ltd. The stock price has fallen by 73% in a single day after the rumored Whatsapp message did its damage on the NSE and wiped nearly Rs. 9200 crores of investor wealth.

The WhatsApp message was about the corporate governance issues of the company, which raised a serious question about the company’s accounting practice. The message was attributed to a brokerage Equirus.

The message said that the company has given an interest-free unsecured loan of Rs. 130 crores to its subsidiary company which has negative assets. The message also speaks about the re-classification of its co-founders based on the shareholding pattern. This has triggered a huge sell-off in the market.

Should You Buy Infibeam Avenues Ltd at this Price?

Well, who doesn’t want to grab this opportunity? It’s a chance for those who are willing to take a risk and play a bet of high-risk high return.

Before betting on, let’s have a look at the company’s financials to check whether the stock is strong enough to bounce back or not. I have written a detailed article on how to do fundamental analysis of the company. check it here.

Infibeam is an e-commerce platform for B2B and B2C. The company is adding around 1500 merchants every month with growing revenue of 100% in the last five years.

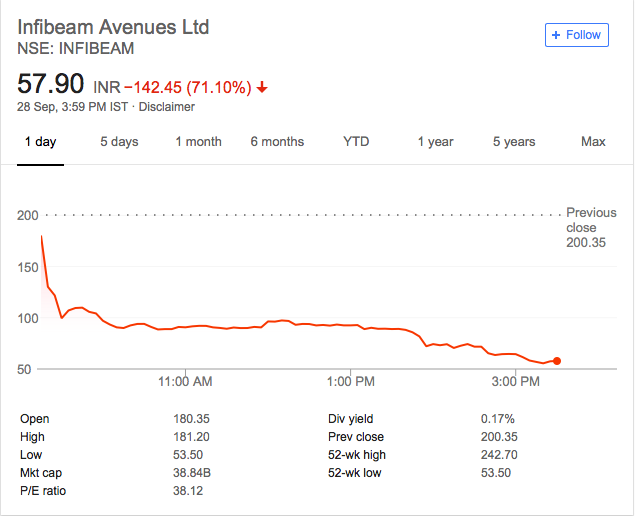

Below are the company’s snapshot and important ratios.

Now let’s have a look at some of the Pros and Cons of the company.

Pros:

- The company is virtually debt free

- Sales growth is 100% in the last 5 years

- The company is expected to give good quarters

- It has positive Operating Profit Margin (OPM)

- Net profit is increasing on a YoY basis

- Compound sales growth of 5 years is 40%

- The company has reserves of Rs. 2588 Crores

- The company is paying tax

- Majority of the cash flow is from operating activity

Cons:

- Promoter’s stake has decreased

- Low return on equity (ROE) of 4.92% in the last 3 years

- The company is capitalizing on the interest cost

As you can see the company is making a profit since last three years. The profit is increasing many folds since last three years.

Fundamentals are looking ok as of now, but the sentiment is bad. BSE has sought the clarification on the news. Further DNA has published a news that the chief financial officer (CFO) of the company has resigned.

In response to the DNA’s news the company has given a clarification that the CFO has not resigned and is performing his duty as it is.

Today in the annual general meeting of the company Mr. Vishal Mehta (Managing Director) has given his speech about the continued growth and future planning. He also has spoken about the WhatsApp rumor and given his assurance to the shareholders that the company is healthy and is working towards the constant improvement which will benefit its shareholders.

Conclusion:

The fundamentals of the company look good and improving year on year. Due to the Whatsapp rumor, the share price has drastically gone down. It is expected to do well in the coming days. But be cautious as the market sentiment is not in favor of the company. If you are willing to take a very high risk, then only try your luck at this time.

People only look at p&l they don’t check balance sheet.

Mr. Market is always right.

P&L looks good, but the sentiment is bad as of now. Let’s wait and watch!